Markets

Where Investors Put Their Money in 2018

Where Investors Put Their Money in 2018

For most investors, 2018 was both an eventful and frustrating year.

Between the looming threat of trade wars and growing geopolitical uncertainty, the market also skipped a beat. Volatility took center stage, and the S&P 500 finished in negative territory for the first time in 10 years.

Although many asset classes finished in negative territory, a look at fund flows – essentially where investors put their money – helps paint a more intricate picture of the year for investors.

Visualizing 2018 Fund Flows

Today’s infographic comes to us from New York Life Investments, and it visualizes the flows in and out of U.S. funds for 2018.

It not only shows when investors poured money into mutual funds or ETFs, but it also breaks down these funds by various categorizations. For example, when did people buy funds that held U.S. equities, and when did they buy funds that primarily held money market securities?

Let’s dive into the data, to take a deeper look.

Mutual Funds vs. ETFs

For another year in a row, ETFs gained ground on mutual funds:

| Type of Fund | 2018 Fund Flows | Total Assets (End of Year) |

|---|---|---|

| ETFs | +$238.4 billion | $3.4 trillion (17.2%) |

| Mutual Funds | -$91.3 billion | $16.3 trillion (82.8%) |

However, despite growing for another year, ETFs still make up a smaller part of the overall fund universe.

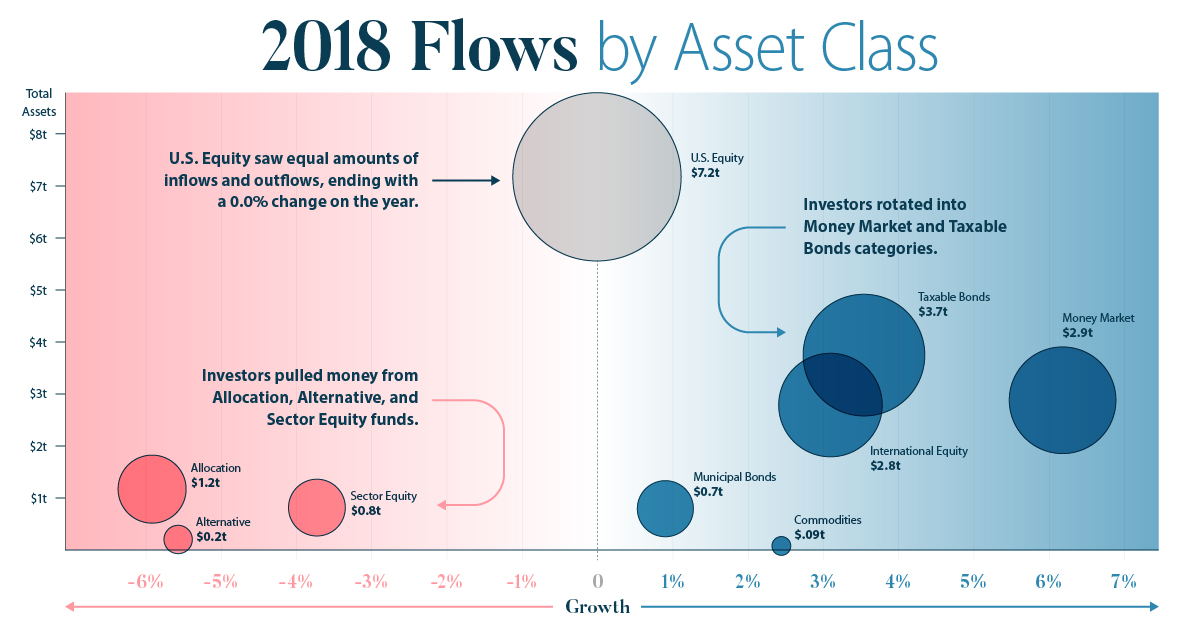

Flows by Asset Class Group

Every fund gets classified by Morningstar based on the types of assets it holds.

For example, a fund that focuses on holding fast-growing, large tech companies in the U.S. would be classified broadly as “U.S. Equity”, and more specifically as “U.S. Equity – Large Growth”.

Here’s how flows went, within these broader groups:

| Fund Category Group | Total Assets ($mm) | Growth in 2018 |

|---|---|---|

| Allocation | $ 1,171,166 | -5.9% |

| Alternative | $ 203,343 | -5.7% |

| Commodities | $ 88,939 | 2.4% |

| International Equity | $ 2,787,400 | 3.1% |

| Money Market | $ 2,879,510 | 6.2% |

| Municipal Bonds | $ 795,132 | 0.9% |

| Sector Equity | $ 816,149 | -3.7% |

| Taxable Bonds | $ 3,747,268 | 3.5% |

| U.S. Equity | $ 7,173,902 | 0.0% |

Investors pulled money from Allocation, Alternative, and Sector Equity funds, while rotating into Money Market and Taxable Bonds categories. These latter assets are considered safer, and this shift is not surprising considering the market volatility towards the end of the year.

Also interesting here is that U.S. Equity – the biggest category overall by total assets – saw equal amounts of inflows and outflows, ending with a 0.0% change on the year.

U.S. Equity: A Closer Look

U.S. Equity ended the year with zero change, but it’s also the biggest and broadest category.

Let’s break it down further – first, we’ll look at what happened to flows by market capitalization (small, mid, and large cap stocks):

| Market Capitalization | Assets | Growth (2018) |

|---|---|---|

| Large Caps | $5.6 trillion | 0.2% |

| Mid Caps | $884 billion | -2.5% |

| Small Caps | $672 billion | 1.7% |

Investment in funds that held large cap stocks increased by 0.2%, while the money allocated to small caps rose by 1.7% over 2018. Interestingly, investors pulled money out of mid caps (-2.5%).

Now, let’s look at U.S. Equity by type of strategy:

| Fund Strategy | Assets | Growth (2018) |

|---|---|---|

| Growth | $2.0 trillion | -2.1% |

| Value | $1.4 trillion | -2.8% |

| Blend | $3.8 trillion | 2.2% |

According to these flows, investors pulled money from funds focused solely on value or growth, while instead preferring funds that were a blend of the two strategies.

International Equities

Finally, let’s see the types of international funds that investors bought and sold over 2018.

| Region | Growth (2018) |

|---|---|

| China | 35.5% |

| Diversified Emerging Markets | 4.9% |

| Latin America | 4.3% |

| Foreign/World | 3.9% |

| Diversified Asia/Pacific | -5.6% |

| Pacific/Asia ex-Japan | -7.1% |

| Japan | -9.0% |

| India | -11.3% |

| Europe | -23.4% |

Investors eschewed funds that had a primary focus on European, Indian, and Japanese markets, while piling into funds that held Chinese equities. Meanwhile, Latin America and emerging markets also got some love from investors.

Conclusion

While 2018 was an eventful year for markets, this recap shows that investors are adjusting their portfolios accordingly.

Where will investors put their money in 2019?

Maps

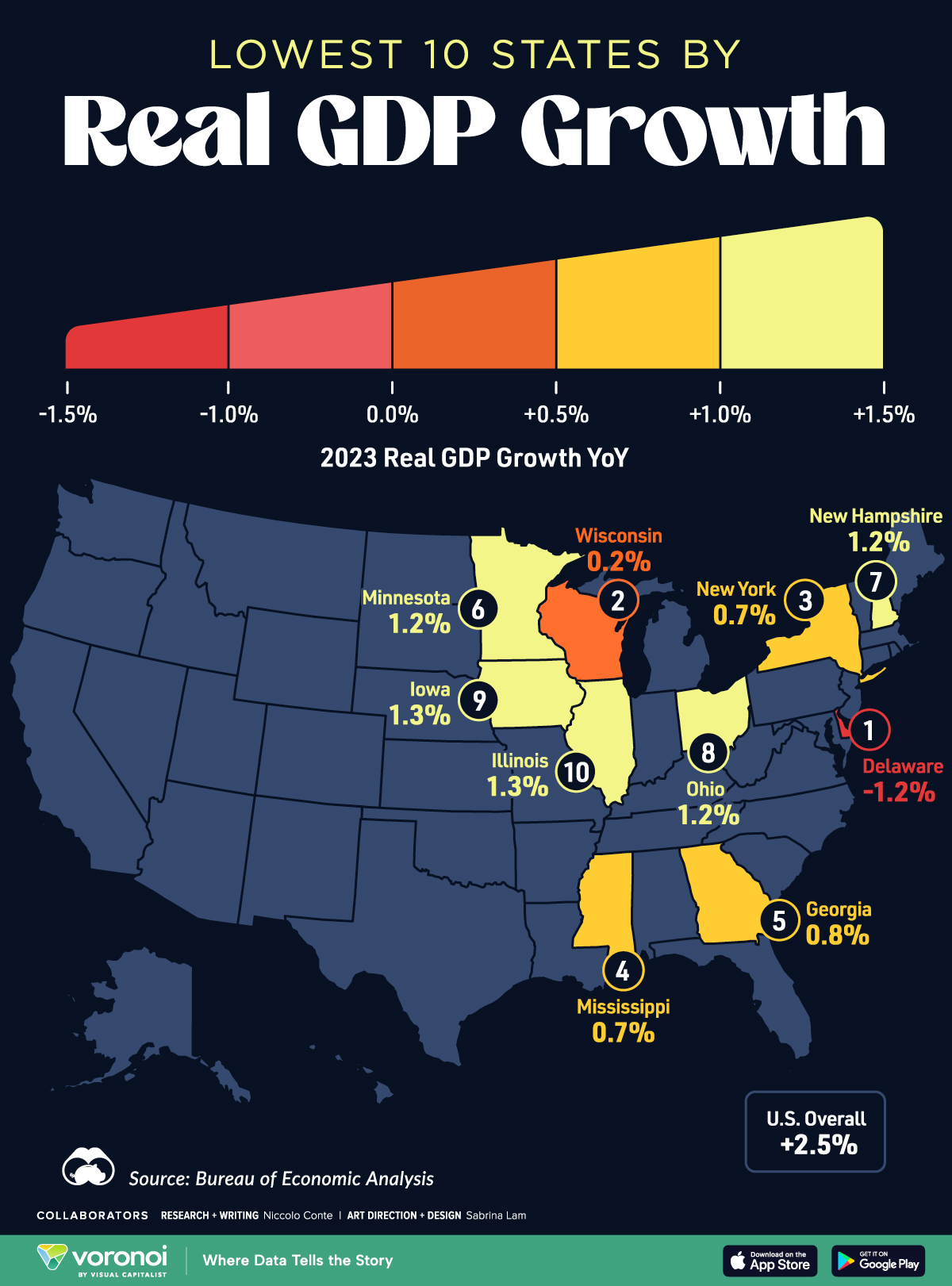

Mapped: The 10 U.S. States With the Lowest Real GDP Growth

In this graphic, we show where real GDP lagged the most across America in 2023 as high interest rates weighed on state economies.

The Top 10 U.S. States, by Lowest Real GDP Growth

This was originally posted on our Voronoi app. Download the app for free on iOS or Android and discover incredible data-driven charts from a variety of trusted sources.

While the U.S. economy defied expectations in 2023, posting 2.5% in real GDP growth, several states lagged behind.

Last year, oil-producing states led the pack in terms of real GDP growth across America, while the lowest growth was seen in states that were more sensitive to the impact of high interest rates, particularly due to slowdowns in the manufacturing and finance sectors.

This graphic shows the 10 states with the least robust real GDP growth in 2023, based on data from the Bureau of Economic Analysis.

Weakest State Economies in 2023

Below, we show the states with the slowest economic activity in inflation-adjusted terms, using chained 2017 dollars:

| Rank | State | Real GDP Growth 2023 YoY | Real GDP 2023 |

|---|---|---|---|

| 1 | Delaware | -1.2% | $74B |

| 2 | Wisconsin | +0.2% | $337B |

| 3 | New York | +0.7% | $1.8T |

| 4 | Missississippi | +0.7% | $115B |

| 5 | Georgia | +0.8% | $661B |

| 6 | Minnesota | +1.2% | $384B |

| 7 | New Hampshire | +1.2% | $91B |

| 8 | Ohio | +1.2% | $698B |

| 9 | Iowa | +1.3% | $200B |

| 10 | Illinois | +1.3% | $876B |

| U.S. | +2.5% | $22.4T |

Delaware witnessed the slowest growth in the country, with real GDP growth of -1.2% over the year as a sluggish finance and insurance sector dampened the state’s economy.

Like Delaware, the Midwestern state of Wisconsin also experienced declines across the finance and insurance sector, in addition to steep drops in the agriculture and manufacturing industries.

America’s third-biggest economy, New York, grew just 0.7% in 2023, falling far below the U.S. average. High interest rates took a toll on key sectors, with notable slowdowns in the construction and manufacturing sectors. In addition, falling home prices and a weaker job market contributed to slower economic growth.

Meanwhile, Georgia experienced the fifth-lowest real GDP growth rate. In March 2024, Rivian paused plans to build a $5 billion EV factory in Georgia, which was set to be one of the biggest economic development initiatives in the state in history.

These delays are likely to exacerbate setbacks for the state, however, both Kia and Hyundai have made significant investments in the EV industry, which could help boost Georgia’s manufacturing sector looking ahead.

-

United States1 week ago

United States1 week agoMapped: Countries Where Recreational Cannabis is Legal

-

Healthcare2 weeks ago

Healthcare2 weeks agoLife Expectancy by Region (1950-2050F)

-

Markets2 weeks ago

Markets2 weeks agoThe Growth of a $1,000 Equity Investment, by Stock Market

-

Markets2 weeks ago

Markets2 weeks agoMapped: Europe’s GDP Per Capita, by Country

-

Money2 weeks ago

Money2 weeks agoCharted: What Frustrates Americans About the Tax System

-

Technology2 weeks ago

Technology2 weeks agoCountries With the Highest Rates of Crypto Ownership

-

Mining2 weeks ago

Mining2 weeks agoWhere the World’s Aluminum is Smelted, by Country

-

Personal Finance2 weeks ago

Personal Finance2 weeks agoVisualizing the Tax Burden of Every U.S. State